.webp)

BLOG

Insights, Strategies, & Expert Guidance for Equipment Industry Professionals

Market Insights

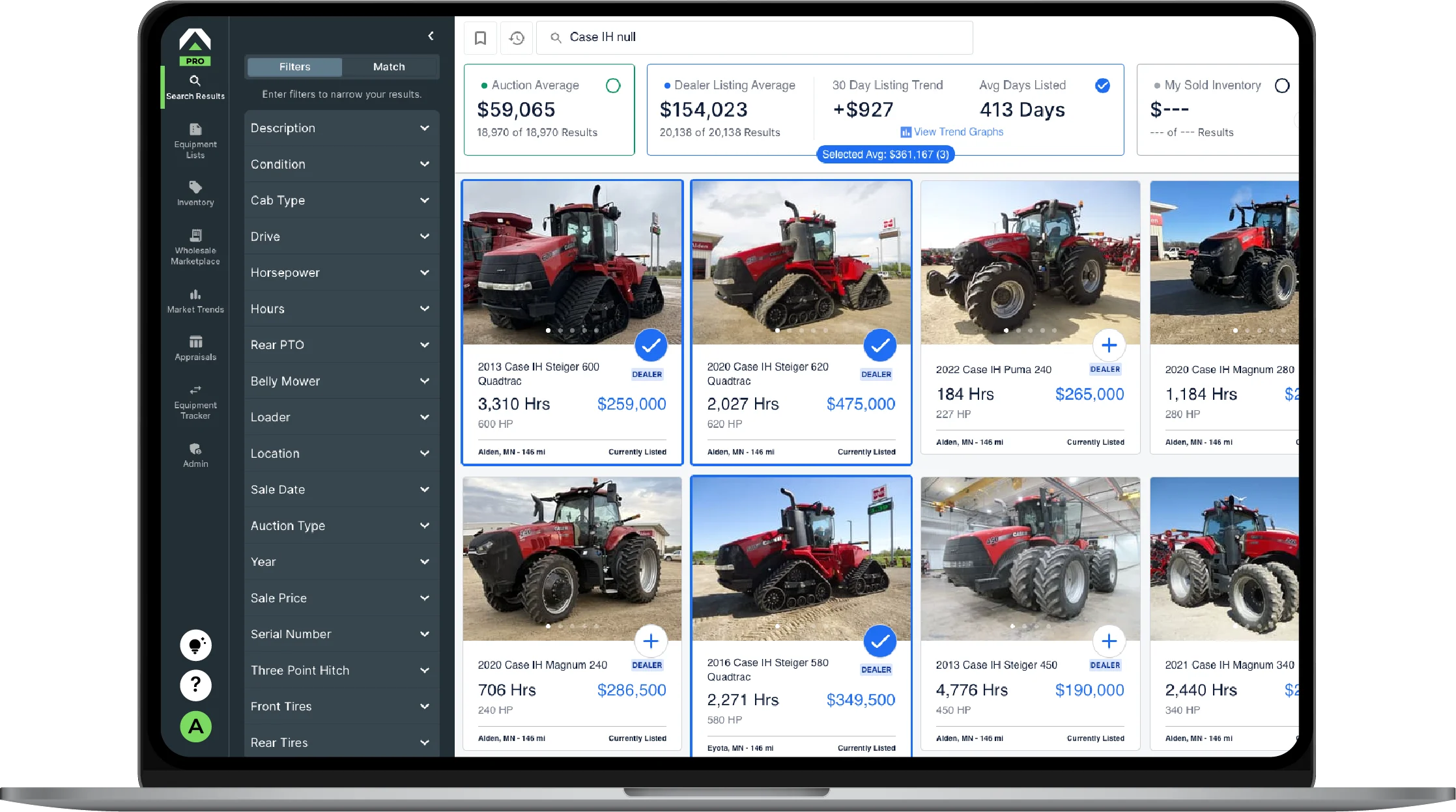

Equipment Market Update: February 2026 Trends Across Categories

26 March 2026

Blogs

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

.webp)

Dealer Playbook: What Top John Deere Dealers Are Doing Differently Right Now

02 March 2026

.webp)

Market Insights

Equipment Market Insights: January Trends Across Tractors, Combines, & Sprayers

25 February 2026

Product & Learning

Quoting Without PDFs: Find OEM Program Data Directly in Anvil Pro

09 February 2026

Market Insights

Early 2026 Equipment Markets: Categories Poised for a Move

29 January 2026

Market Insights

2025 Year-End Equipment Market Summary & Key Trends in 2026

23 December 2025

Tractor Zoom Updates

How Customers & Partnerships Shaped Tractor Zoom’s 2025 Milestones

22 December 2025

Performance & Strategy

Always Be Improving: What’s Next for Tractor Zoom and the Dealers We Serve

28 October 2025

Performance & Strategy

Exploring the Value of Used Equipment Warranties in Resale

21 October 2025

Market Insights

Fall 2025 Equipment Market Report: Key Takeaways

15 October 2025

Performance & Strategy

Equipment Velocity Guide: How Slow Movement Impacts Margins

08 September 2025

Market Insights

Summer 2025 Combine & Header Market Analysis

21 August 2025

Tractor Zoom Updates

Tractor Zoom Pro Now Available as a Solution for AGCO's Dealer Network

19 August 2025

Performance & Strategy

Why Your Dealership Needs a Data Strategy to Stay Competitive

18 August 2025

Product & Learning

Conquer Operational Challenges With a Dealer Intelligence Platform

18 August 2025

Performance & Strategy

Building Trust and Transparency Around Your Data

15 August 2025

No Results.

Please try again.

Videos

Embracing AI and Data in Parts Management | Wayne Brozek

February 9, 2026

Inside Tractor Zoom | 2025 Growth

October 28, 2025

Unlocking the Value of Warranty in Equipment Sales | Jacob Bryce

September 22, 2025

Transforming Equipment Dealerships That Last | George Keen

May 22, 2025

Aged Inventory Challenges & Data Utilization | George Keen

May 5, 2025

Enhanced Sales Management for Dealers | George Keen

May 5, 2025

Texas Tough: Moving Equipment After Hurricanes & Economic Downturn | Brad Crist

December 18, 2024

Titan Machinery Used Equipment Management in 2024 & Beyond | Don Aberle

November 13, 2024

AGCO Used Equipment Outlook in the Southeast | John Hoffmann

October 30, 2024

Data Strategy 101 for Equipment Dealers | Timothy Johnson

October 7, 2024

Kubota Dealer & Technology Leader River Valley Tractor | Taylor Carlow

September 13, 2024

A Farmer's Perspective: Building Relationships with Dealers | Quentin Connealy

August 26, 2024

Farmer Buying Behavior: What Dealers & Lenders Need to Know | Brady Brewer

August 1, 2024

Leo Johnson: Dealership Succession Planning & Growth Through Acquisitions

July 19, 2024

Jim Rothermich: Land and Machinery Trends, Data, and Future Prospects

July 5, 2024

Van Wall & Vesel: Hiring Strategy & Talent Development for Dealerships

June 19, 2024

Duane Kautzman: Dealership Strategies for a Slower Farm Economy

June 7, 2024

Hank Mandsager: Leveraging AI as “Actionable Insights” for Dealerships

May 23, 2024

Pilot Episode: What Lies "Beyond the Hood"

May 23, 2024

Jason Hoult: Implementing Gradual Growth at Dealerships

May 23, 2024

Ivan and Brandon Dorhout: Developing Your Workforce and Planning for Succession

May 23, 2024

J.D. Marbury: Equipment Export Processes & Crazy Stories Abroad

May 23, 2024

Jeff Oldham: Leading a Dealership Culture of Innovation

May 23, 2024

Join the future of ag & heavy equipment sales

Take a guided tour of Tractor Zoom Pro and Anvil Pro to discover how wider margins and faster turns are just a few clicks away.